Key Points

- The proposed interim budget totals $14.7 million across two funds: $10 million in the general fund and $4.725 million in the Highway Users Revenue Fund.

- Nearly $7 million of the general fund sits in a non-departmental contingency line. Staff said the town will be conservative with spending.

- The town has roughly $12 million in the bank but cannot spend any of it until the council formally adopts a budget. In the meantime, the town has borrowed $1.405 million from Queen Creek at $1,200 in interest to cover startup costs.

- Target date for adoption is April 1, 2026. Once adopted, the budget would take effect the following day.

SAN TAN VALLEY, AZ — The San Tan Valley Town Council reviewed a proposed interim budget totaling $14.7 million during a special work session on Feb. 19, 2026. Finance Consultant Bill Kauppi of Pat Walker Consulting presented the spending plan. According to Kauppi, the budget would allow the newly incorporated town to begin spending its own revenue. No formal action was taken at the meeting. Council members asked questions and received an overview of the budget’s structure, timeline, and key expenditures.

Why the Town Needs an Interim Budget

San Tan Valley incorporated partway through the current fiscal year. According to Kauppi, Arizona cities normally adopt budgets in June or July for the coming year. However, because the town formed mid-cycle, state law provides a different path.

Arizona Revised Statute 42-17110 allows a newly incorporated city or town to adopt an interim budget by ordinance for the remainder of the fiscal year in which it was incorporated. The current fiscal year runs from July 1, 2025, through June 30, 2026. Under the same statute, the interim budget does not constrain the town’s first full-year budget, which Kauppi said would follow the normal adoption process beginning around May or June.

Town Manager Brent Billingsley said, “The reason why an interim budget is important in this capacity is, if we want to begin spending our own money, we have to have a budget before we can do that.”

Kauppi said the town has approximately $11.5 to $12 million in the bank. “But you can’t spend any of it until council formally adopts a budget,” he said. He added that everything presented was a draft. “All of this is subject to change, so it’s very flexible at this point.”

Budget at a Glance: $14.7 Million Across Two Funds

The proposed interim budget covers two funds. Below is the high-level summary Kauppi presented.

| Fund | Estimated Revenues (FY 2025–26) | Estimated Expenditures (FY 2025–26) |

|---|---|---|

| General Fund | $10,000,000 | $10,000,000 |

| Highway Users Revenue Fund (HURF) | $4,725,000 | $4,725,000 |

| Total All Funds | $14,725,000 | $14,725,000 |

Kauppi said he budgeted expenditures equal to estimated revenues to give the town maximum spending flexibility.

General Fund Revenue: What’s Coming In

Kauppi presented the following general fund revenue actuals as of Jan. 29, 2026, alongside the proposed interim budget estimates.

| Revenue Source | Actuals as of 1/29/2026 | Interim Budget FY 2025–26 |

|---|---|---|

| State Sales Tax | $5,856,471 | $7,500,000 |

| Vehicle License Tax | $1,841,880 | $2,500,000 |

| Urban Revenue Sharing | – | – |

| Interest / Local Gov’t Investment Pool | – | – |

| Total General Fund Revenues | $7,698,311 | $10,000,000 |

Kauppi explained that urban revenue sharing, the income tax component, cannot be collected mid-fiscal year. He said the town will begin receiving those funds starting July 1. He also said the council should consider adopting an investment policy, noting that roughly $12 million is sitting in the bank earning only bank credit.

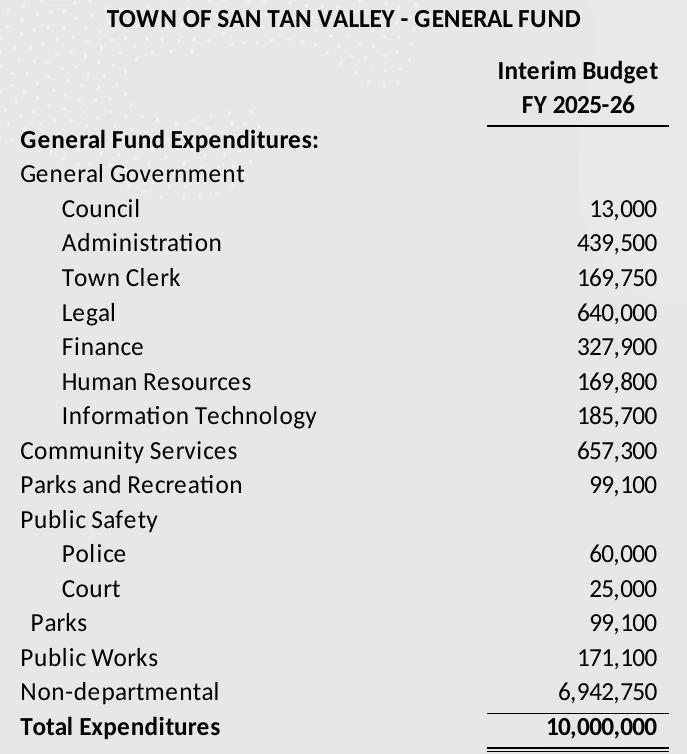

General Fund Expenditures by Department

The proposed general fund breaks down into departmental estimates.

Nearly $7 million sits in the non-departmental line as contingency. Kauppi said revenue not allocated to specific departments is held there and can be moved into departments as needs arise.

Billingsley said the budgeted amount does not represent planned spending. “We’re going to be conservative on our expenditures, but in case we have things that come up that we’re not planning for, we want to have capacity for contingency,” he said.

Software, Elections, and Other Estimated Expenses

Billingsley told council members that the town used its best estimates of known expenses, “but some things aren’t known at this point.”

He said some of the upcoming expenditures will be “tremendously expensive,” citing finance software, permitting software, and HR software as examples. “Until we actually bid that and/or find cooperative contracts to make those purchases, we don’t know,” he said. Kauppi said he included software line items in several departments, though he noted he would need to double-check whether HR had one yet.

Billingsley also listed zoning codes, municipal code development, and a floodplain ordinance as upcoming expenses. He said election mail-outs are another cost the town did not initially anticipate. “Probably over $100,000 just for election mail-outs, where we have to have them printed and have a company do the election mailers,” he said.

According to the presentation, the budget also includes 13 proposed staff positions, legal services, and vehicle purchases. Kauppi said the budget includes about four or five vehicles and various organizational memberships.

Spending Limits and What Happens to Unspent Funds

Kauppi outlined the rules governing the San Tan Valley interim budget. He said that even if the town collects $11 million in revenue, it can only spend up to the $10 million budgeted on the general fund side. That cap applies to the expenditure side, not the revenue side, he said.

However, Kauppi said money that goes unspent does not disappear. He told the council that unused funds carry forward into the next budget year. “It’s not like if I don’t spend it, I lose it,” he said. “You don’t spend it, it just rolls into next budget year. You just reappropriate it.”

The Highway Users Revenue Fund

According to Kauppi, the HURF portion of the budget totals $4.725 million. He explained that these funds are restricted to street-related expenses such as pavement maintenance and street lights. He added that the town will likely need to enter an intergovernmental agreement with the county for that work initially.

Borrowing From Queen Creek: $1.4 Million at $1,200 in Interest

According to Billingsley, the town has been borrowing from the Town of Queen Creek to cover startup costs.

“We have borrowed, we just checked on this, we just got it today — $1.405 million is what we’ve processed thus far,” Billingsley told the council. “The interest on that is $1,200.”

Kauppi responded: “I do want to point out that that is a really good deal.”

However, Billingsley said this arrangement has limits. He said spending needs will “very quickly” exceed $250,000, and that “the next step” of $450,000 would also fall short. According to Billingsley, Kauppi had already warned that $450,000 would not be enough by May and June. “We need to get over to spending our own money,” Billingsley said, “because pretty soon we’re going to outpace our ability to borrow from Queen Creek.”

Audit and Reporting Requirements

According to Kauppi, the San Tan Valley interim budget does not carry the same administrative requirements as a standard annual budget. He confirmed that Auditor General forms A through G are not required for an interim budget. An annual audit is also not required this year, he said.

That changes once the town completes its first full fiscal year. “When you have a full year and you have to go through this process, an audit will be required,” Kauppi said. He said an independent audit firm would then review the town’s books for compliance.

Paying Bills Without an Accounting System

Council members asked how quickly funds would become available after budget adoption. Kauppi said access would essentially begin the next day. However, he said practical challenges remain.

“We don’t have an accounting system,” he said. He added that the town still needs to work out how it will process payments and manage finances. Adopting the budget itself is “one of the easiest things,” Kauppi noted, but payment logistics and other processes “will have to be worked out.”

Billingsley said the town also currently lacks purchasing policies, which are part of the town code still under development. In the meantime, he said staff plans to use cooperative purchasing contracts. He noted that from his past experience, the town can sometimes get a better price by going out to bid rather than using cooperative contracts, particularly for highly specialized items such as water meters. He said the town will do more of that analysis once it has a procurement person and a completed town code.

Proposed Timeline for Budget Adoption

Allen Quist, the town’s attorney at Pierce Coleman PLLC, said he calculated the adoption timeline based on Pinal Central’s Thursday publication schedule and the required two-week public notice window.

- March 5 or March 19, 2026: Public hearing to receive comments on the proposed interim budget, according to the presentation slides. Quist said the tentative budget would come back to council for review at the next regular meeting. Residents can check santanvalley.gov for confirmed meeting dates.

- April 1, 2026: Target date for a second public hearing and adoption by ordinance. Quist said the two-week publication requirement pushes the earliest possible adoption to this date. “We’re thinking April 1st would probably work,” he said. A special meeting could shave about two weeks off that timeline, he added.

Mayor Daren Schnepf said, “Better to get that adopted as soon as we can.” According to Kauppi, once adopted, the budget would take effect the following day. The town would then have through June 30, 2026 — the end of the fiscal year — to spend under the approved limits.